If you are an NRI, managing your finances in India requires more than just opening a bank account. One of the most important decisions you will make is choosing between an NRE and NRO account. This choice directly impacts your taxation, repatriation ability, and overall FEMA compliance.

Many NRIs unknowingly make mistakes by using the wrong account or mixing funds, which can lead to tax complications and regulatory issues. Understanding NRE vs NRO account NRI is essential to ensure your money is handled in a compliant and efficient manner.

Understanding FEMA Rules for NRI Banking

Under the Foreign Exchange Management Act (FEMA), NRIs must follow specific guidelines when dealing with income earned inside and outside India. These rules are designed to track the source of funds and regulate foreign exchange movement.

Failure to comply can lead to penalties, notices, or even legal complications. That’s why selecting the right account type is not just a financial decision—it’s a compliance requirement.

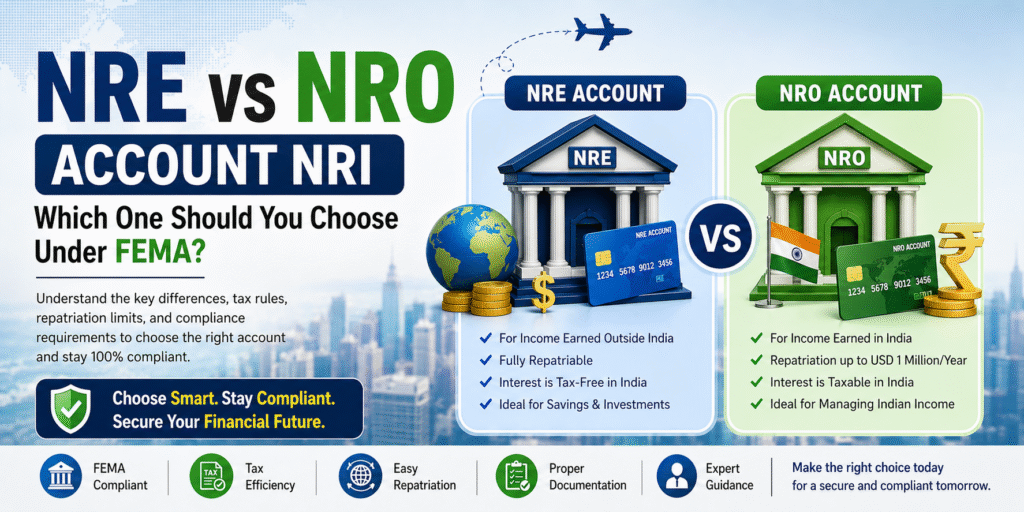

What is an NRE Account?

An NRE (Non-Resident External) account is meant for depositing income earned outside India. This includes your foreign salary, overseas business income, or savings accumulated abroad.

Key Features:

- Funds are fully repatriable without restrictions

- Interest earned is completely tax-free in India

- Maintained in Indian Rupees but sourced from foreign currency

- Helps in easy transfer of funds back to your country of residence

In the NRE vs NRO account NRI comparison, NRE accounts are ideal for NRIs who want flexibility and tax efficiency on their foreign earnings.

What is an NRO Account?

An NRO (Non-Resident Ordinary) account is used to manage income earned within India. This includes rent, dividends, pension, or any other domestic income.

Key Features:

- Repatriation allowed up to USD 1 million per financial year

- Interest is subject to Indian income tax and TDS

- Helps manage local expenses and obligations in India

- Mandatory for handling Indian-source income

When analyzing NRE vs NRO account NRI, NRO accounts are essential for staying compliant with Indian income regulations.

NRE vs NRO Account NRI: Key Differences Explained

Choosing between these two accounts becomes easier when you understand their core differences:

1. Source of Funds

- NRE: Foreign income

- NRO: Indian income

2. Taxation

- NRE: Tax-free interest

- NRO: Taxable interest

3. Repatriation

- NRE: Fully repatriable

- NRO: Limited to USD 1 million annually

4. Purpose

- NRE: Savings and investments from abroad

- NRO: Managing Indian earnings

Understanding these differences in NRE vs NRO account NRI helps you avoid compliance mistakes and optimize your financial planning.

Real-Life FEMA Compliance Example

Let’s take a practical scenario.

Rahul works in the United States and sends part of his salary to India for investment purposes. This money should be deposited into his NRE account.

At the same time, Rahul owns a property in Hyderabad and earns monthly rental income. This income must be deposited into his NRO account.

If Rahul mixes these funds or uses the wrong account, it can create issues under NRE vs NRO account NRI compliance rules, potentially attracting penalties or scrutiny.

Common Mistakes NRIs Make

Many NRIs unknowingly violate FEMA rules due to lack of awareness. Some of the most common mistakes include:

- Depositing Indian income into NRE accounts

- Using savings accounts after becoming an NRI

- Mixing foreign and Indian income in one account

- Ignoring repatriation limits on NRO accounts

- Not updating residential status with banks

Avoiding these mistakes is crucial when dealing with NRE vs NRO account NRI structures.

Why Choosing the Right Account Matters

Selecting the wrong account type is not just a technical error—it can have real financial consequences.

Potential Risks:

- Higher tax liability

- Delays in transferring money abroad

- FEMA compliance notices

- Difficulty in proving the source of funds

- Complications during financial audits

This is why understanding NRE vs NRO account NRI is essential for protecting your wealth and staying compliant.

Smart Compliance Tips for NRIs

To ensure smooth banking and compliance:

- Route all foreign income through NRE accounts

- Deposit Indian income only in NRO accounts

- Avoid mixing funds under any circumstances

- Regularly review your bank accounts

- Keep proper documentation of income sources

For complete peace of mind, consult a FEMA consultant NRI banking expert who can guide you through the process.

How Femabide Advisorz Supports NRIs

Femabide Advisorz specializes in FEMA compliance and NRI banking advisory. We help NRIs:

- Choose the right account structure

- Review and correct existing accounts

- Ensure tax efficiency

- Handle FEMA compliance issues

- Plan repatriation smoothly

Our goal is to simplify complex regulations and provide practical solutions tailored to your needs.

FAQs

1. What is the main difference between NRE and NRO accounts?

NRE accounts are used for foreign income and are tax-free, while NRO accounts are used for Indian income and are taxable.

2. Can I hold both NRE and NRO accounts?

Yes, most NRIs maintain both accounts to manage different income sources efficiently.

3. Is interest earned on NRE accounts taxable?

No, interest on NRE accounts is completely tax-free in India.

4. What is the repatriation limit for NRO accounts?

You can transfer up to USD 1 million per financial year after paying applicable taxes.

5. Can I transfer money from NRO to NRE account?

Yes, but it requires proper documentation and compliance with FEMA rules.