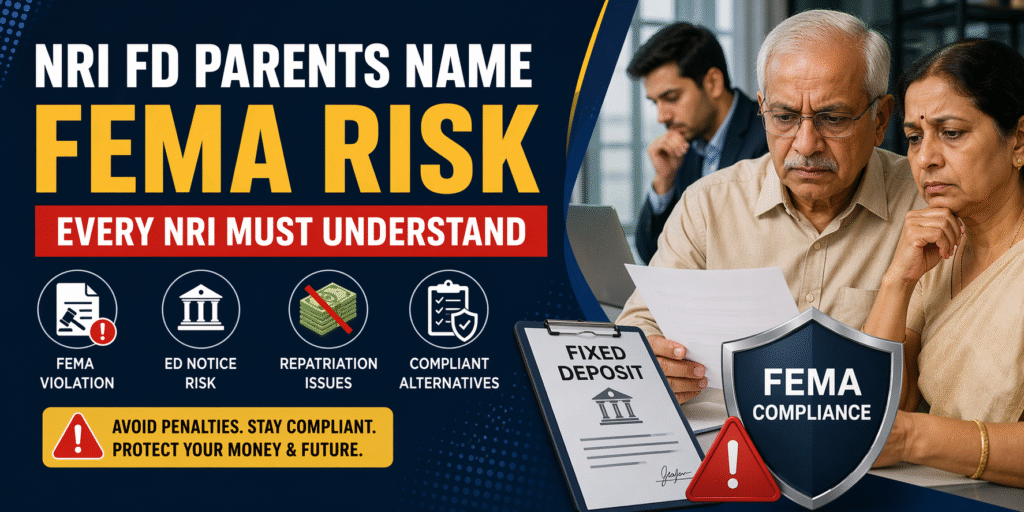

Many NRIs believe that keeping fixed deposits in their parents’ names is a simple and safe financial strategy. While it may look convenient, the NRI FD parents name FEMA issue is becoming a major compliance concern in India. What appears to be a family arrangement can actually lead to serious regulatory consequences if not structured correctly.

Why NRI FD Parents Name FEMA Practice Is So Common

The FEMA situation arises because of practical intentions. NRIs often want to support their parents, manage money easily in India, and sometimes reduce tax liability. However, lack of awareness about FEMA rules leads to incorrect structuring of these deposits.

This common practice is now under increased scrutiny by authorities, making it important for NRIs to understand the risks involved.

NRI FD Parents Name FEMA and FEMA Violation Risk

Under FEMA regulations, transferring large funds to a resident individual and creating fixed deposits in their name can be treated as a compliance violation. The FEMA structure may be classified as:

Unauthorized remittance

Indirect lending to a resident

Improper use of banking channels

This is where many NRIs unknowingly fall into a FEMA violation category.

How NRI FD Parents Name FEMA Can Lead to ED Notice

Authorities like the Enforcement Directorate monitor high-value transactions involving NRIs. The NRI FD parents name FEMA issue becomes serious when transactions are flagged during scrutiny.

Possible consequences include:

Show cause notice under FEMA

Heavy financial penalties

Freezing of bank accounts

Legal proceedings for both NRI and parents

An ED notice in India can come years after the transaction, which makes this risk even more dangerous.

FEMA and Repatriation Problems

Apart from compliance risk, the NRI FD FEMA structure creates long-term financial complications.

NRIs may face:

Difficulty in repatriating funds abroad

Inheritance disputes after parents’ lifetime

Complex documentation requirements

Tax issues on inherited deposits

This turns a simple financial decision into a complicated legal situation.

NRI FD Parents Name FEMA Safe Alternatives for Compliance

To avoid the FEMA risk, NRIs should follow compliant investment options.

Use NRE fixed deposits which are fully repatriable and tax-free

Choose FCNR deposits to avoid currency risk

Keep NRI funds separate from resident accounts

Ensure proper documentation and nomination

These options are designed specifically to maintain FEMA compliance for NRI investments.

Why NRI FD Parents Name FEMA Needs Expert Review

Many NRIs assume their structure is safe because no issue has occurred yet. However, the NRI FD parents name FEMA problem usually appears later during audits or investigations.

Consulting a FEMA expert helps:

Identify hidden compliance risks

Correct existing FD structures

Avoid penalties and legal issues

Ensure smooth repatriation in the future

FAQs

Is NRI FD parents name FEMA allowed in India

No, it is risky if not structured properly and can lead to FEMA violations.

Can NRIs transfer money to parents legally

Yes, but using that money for investments like FDs without compliance can create issues.

What is the safest FD option for NRIs

NRE and FCNR deposits are the safest and fully compliant options.

Can NRI repatriate money from parents account easily

No, repatriation is complex and involves strict documentation.

What happens if FEMA violation is detected

Penalties, account freezing, and legal action may follow.

How to avoid NRI FD parents name FEMA risk

Use proper NRI accounts, avoid mixing funds, and consult a FEMA expert.

Conclusion

The NRI FD parents name FEMA issue is one of the most overlooked compliance risks today. With increasing regulatory checks, NRIs must ensure that their financial arrangements are fully compliant rather than convenient.