In an increasingly globalized world, overseas remittances by resident Indians—for education, family support, or long-term financial planning—have become routine. However, what appears to be a well-intentioned and convenient transfer can quickly escalate into a serious regulatory breach if compliance requirements are overlooked.

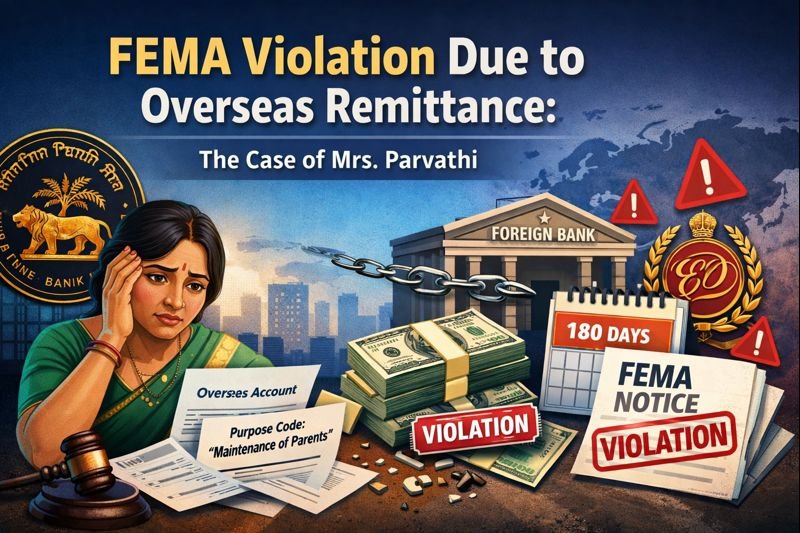

The case of Mrs. Parvathi, a resident Indian, illustrates how genuine intentions can still result in significant violations under the Foreign Exchange Management Act (FEMA), leading to penalties, adjudication, and legal scrutiny.

Background of the Case

Mrs. Parvathi remitted approximately USD 2.5 lakh annually for her newborn daughter’s future financial security abroad. Over a period of 15 years, these remittances accumulated into a substantial amount.

While the objective was lawful, two major compliance lapses under FEMA and RBI regulations ultimately exposed her to severe consequences.

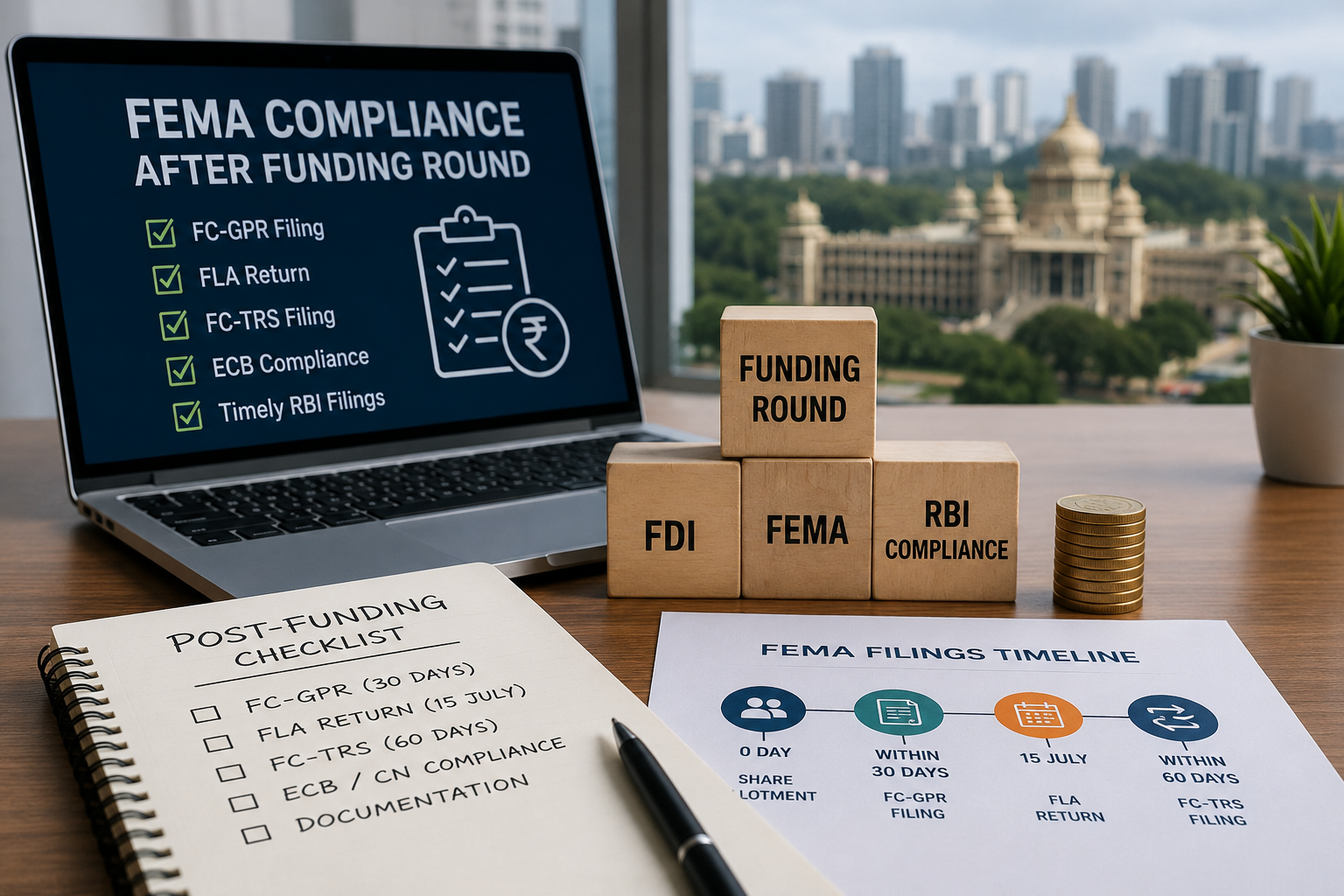

Understanding the FEMA and LRS Framework

Under the Liberalised Remittance Scheme (LRS), resident Indians are permitted to remit up to USD 250,000 per financial year for permissible current or capital account transactions, as governed by FEMA, 1999.

Mrs. Parvathi routed her remittances under LRS. However, a critical error occurred when she declared the purpose of remittance as “maintenance of parents”, while the actual intent was long-term savings for her child.

As per Reserve Bank of India guidelines, every outward remittance must carry an accurate purpose code. Any mismatch between the declared purpose and the actual intent is treated as misrepresentation, triggering red flags under FEMA’s disclosure and reporting framework.

The Second FEMA Breach: Non-Repatriation of Funds

A more serious contravention arose when the remitted funds remained unutilized in a foreign bank account for more than 180 days.

Under FEMA and LRS regulations:

- If funds are not used for the declared purpose within 180 days, they must be repatriated to India.

- Retaining unutilized funds overseas beyond this period is considered unauthorized capital retention.

In Mrs. Parvathi’s case, repeated non-repatriation over 15 years resulted in a multi-crore exposure, significantly aggravating the violation and attracting potential scrutiny from the Enforcement Directorate.

Why FEMA Non-Compliance Is a Serious Risk

FEMA violations are not treated as minor procedural lapses.

Under Section 13 of FEMA:

- Penalties can extend up to three times the amount involved in the contravention.

- Based on current exchange rates, Mrs. Parvathi’s potential exposure is estimated at ₹30 crore.

While RBI provides a compounding mechanism for certain first-time or technical violations, repeated or long-term non-compliance often leads to:

- Adjudication proceedings

- ED investigations

- Freezing of accounts

- Seizure of assets

Key Compliance Lessons from Mrs. Parvathi’s Case

1. Use the Correct Purpose Codes

Always declare the exact RBI-prescribed purpose code (e.g., S1302 for gifts). Incorrect declarations are treated as misrepresentation under FEMA.

2. Track Utilisation Timelines

Ensure remitted funds are utilized within 180 days. If not, repatriate the amount to India without delay.

3. Stay Within LRS Limits

The USD 250,000 annual cap under LRS must be strictly adhered to. Any excess requires prior RBI approval.

4. Maintain Robust Documentation

Preserve:

- Income proofs

- Bank statements

- Remittance advice

- Intent and utilisation records

These are critical during audits and investigations.

5. Seek Professional FEMA Guidance

Engage experienced FEMA and forex compliance consultants to structure overseas remittances correctly and lawfully.

The Real Takeaway: Convenience Is Not Compliance

FEMA is not designed to restrict genuine overseas transfers—it exists to ensure transparency, traceability, and lawful foreign exchange management.

Mrs. Parvathi’s 15-year oversight highlights a crucial reality:

Convenience does not equal compliance.

Even well-meaning shortcuts or informal practices can result in severe penalties under FEMA and RBI regulations. With proper planning, accurate disclosures, and expert guidance, resident Indians can support their families abroad without risking legal consequences.

Staying informed, compliant, and professionally advised is the only sustainable way to manage overseas remittances under FEMA.